Portfolio Update #7

"Though we may not have reached the heights we anticipated yesterday, today is a brand new day to begin a new climb." - Chinonye J. Chidolue

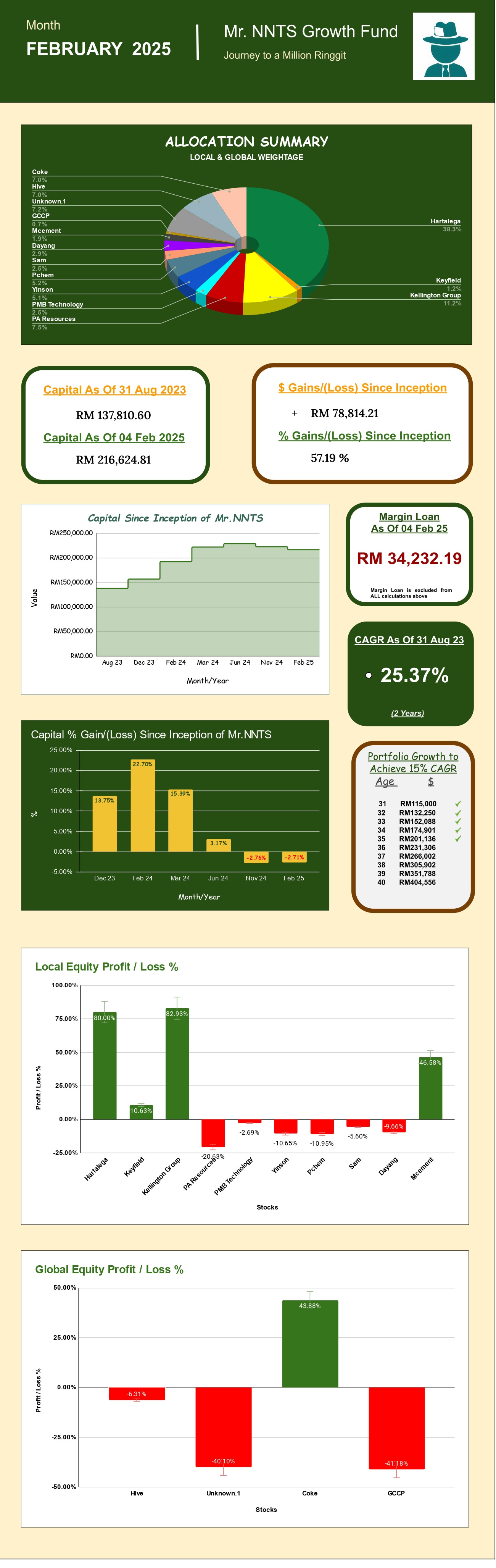

In the blink of an eye, February 2025 has already arrived. Time seems to have flown by, and during this period, I’ve been busy revisiting and updating my portfolio, while also giving some thought to refreshing the format of my blog.

Looking back on the market, it's undeniable that the journey so far has been anything but smooth. The volatility we've seen across various sectors has created both challenges and opportunities. One of the most significant factors influencing the market, in my opinion, is the series of ongoing "wars"—a broad term I use to describe several geopolitical, financial, and digital rivalries currently shaping the world. These include the Russia vs. Ukraine conflict, the battle between Bitcoin and Gold for dominance in the digital and traditional asset space, and perhaps most importantly, the ongoing tariff war that has escalated under Trump’s policies. The latter, in particular, has the potential to create ripples across the global economy, with far-reaching consequences for trade, investments, and international relations.

In light of these developments, I’ve decided to make slight adjustments to my portfolio. While I continue to pursue capital growth through stocks, I’ve shifted toward a more defensive approach to safeguard against potential market turbulence. This shift involves selectively diversifying into more resilient sectors and assets, positioning myself to weather the uncertainty while still aiming for long-term growth. The goal is to balance the pursuit of returns with the need for stability in an unpredictable environment. As the market continues to evolve, I’ll be staying vigilant and ready to adapt further if necessary.

The Portfolio Update

As I brace for 2025, I’ve made some adjustments to my portfolio, particularly due to the stock market downturn, which seems to have been triggered by Trump’s return to the White House. The ongoing tariff war remains uncertain, so I’ve reduced some holdings and shifted towards holding more cash, giving me the flexibility to utilize margin when the market crash hits. When it does, I’ll be ready to pick up potential bargains.

The global market trend continues to focus heavily on AI development, especially within the Technology and Software sectors. Despite this, I’ve made only small changes to my Global Portfolio—mainly reducing some Hive holdings to top up on Unknown 1. I’m still optimistic about Hive’s potential for exponential growth, believing it’s about time for a significant rise, assuming the cycle follows past patterns. Only time will tell what unfolds throughout 2025. In the worst case, I’m aiming to break even and keeping an eye on a few stocks on my watchlist. The semiconductor sector has been hit hard recently, and I’m hoping for further pullbacks so I can capitalize on the discounts when the time is right.

I have made small changes to the Local Portfolio going into 2025 .Feng shui dictates that the year of the Snake seems to be a good & prosperous year for me financially and I hope it comes true. Locally construction sector is in the hots for the invigoration of the industry by the government by approving mega projects such as MRT Line 3 (Circle Line), East Coast Rail Link (ECRL), Klang Valley LRT 3 (LRT3), Penang Transport Master Plan (PTMP) & KLIA Aeropolis which mainly benefits Malayan Cement. However, I’ve decided to reduce my position to lower levels in order to make room for other opportunities I've identified. Lets not forget about the Data Centre FDI that has been piling into the country recently which gave rise to stocks related to its industry. I have profited from the investment in Southern Cable Group albeit it could have been more but I am satisfied with it. However, with the discounts incoming I do hope to get a chance to nibble onto YTL Power if it comes downs to my desired price.

Since my last update in November 2024, I’ve made some adjustments to my portfolio. I’ve sold portions of Hartalega, Keyfield, and Malayan Cement, and used the proceeds to add Petronas Chemical, Dayang, and SAM Engineering, while also increasing my position in PA & Yinson.

Hartalega remains my top holding. With the ongoing tariff impact, I anticipate a significant increase in their profits. While it’s true that China’s glove business could shift away from the U.S. to other markets, I believe Hartalega's strong fundamentals and position as one of the top four glove manufacturers still give it a competitive edge. I’m optimistic that Hartalega will eventually return to paying dividends at pre-COVID levels, and I foresee further potential for its share price to appreciate. PA Resources is another stock I believe will benefit from the U.S. tariffs imposed on Malaysia, as they’ve managed to secure a duty exemption for their products sold to the U.S. First Solar remains their largest and top customer. Progress is going well with the construction of their new factory, and I’m confident that their earnings will see a substantial increase once it’s completed and fully operational.

Dayang, a recent addition to my local stock portfolio, operates in the same sector as Keyfield, making them competitors. However, I opted to invest more in Dayang due to its improved earnings visibility. The company’s strong performance is backed by recent multi-year contract wins, which have boosted its order backlog to RM5.3 billion. These contracts, primarily in topside maintenance for oil majors and offshore support vessel services, position Dayang well for continued growth. With impressive quarterly net profit margins of 28-30%, I see potential for short-term gains and am confident in the opportunity to potentially double my investment.

SAM Engineering is a leading player in the engineering and manufacturing sectors, with a focus on aerospace, automation, and precision engineering. The company has a strong order book and continues to secure high-value contracts, particularly in industries driven by technological advancement and automation. Looking ahead, SAM’s involvement in the aerospace and automation sectors positions it well to benefit from ongoing trends in these industries, potentially driving growth in the medium to long term. Its solid fundamentals and expanding market opportunities make it an interesting stock to watch for future gains.

I recently added SAM Engineering into my portfolio after it hit around RM4, which I consider a solid support price based on technical analysis. While I’m unsure how long I’ll hold it, I’m looking to sell between RM6-RM8 to lock in gains and make room for my next big target, Petronas Chemical (Pchem). The stock's potential upside, coupled with its strong market position, makes it a short-to-medium term play that fits well with my strategy.

I decided to increase my position in Yinson, aligning with my strategy of investing in companies with strong future growth potential. Recently the company has set to raise up to US$1.15 billion through the issuance of Redeemable Convertible Preference Shares (RCPS), a move that will significantly strengthen its capital reserves. This capital raise is vital for funding Yinson’s ambitious projects, especially in the renewable energy and offshore oil & gas sectors. A key partner in this expansion is the Abu Dhabi Investment Authority (ADIA), which adds credibility and further growth opportunities to Yinson’s portfolio.

Now, the focus is on how effectively Yinson’s management will deploy this fresh capital to secure high-return projects and drive long-term growth. I’m closely monitoring their cash flow, particularly with their vessels now involved in oil production, as these operations are expected to generate steady revenue streams and improve their financial outlook in the near future.

Why I’m Going Big Into Petronas Chemicals (Pchem)

After closely analyzing the market, I’ve decided to start a small position in Petronas Chemicals (Pchem), with plans to increase it significantly, making it my next top holding behind Hartalega. As a government-linked company, Pchem’s massive size and contribution to the Malaysian economy make it a key player, and its performance directly impacts the nation’s financial health. If Pchem were to struggle, it could have far-reaching effects on the economy, given its scale.

Despite the current overselling in the industry, Pchem has managed to maintain profitability, which sets it apart from other players in the sector. For example, LC Titan has been posting losses for the past two years, whereas Pchem has shown resilience, continuing to generate profits. This stability is a testament to Pchem’s strong fundamentals and ability to navigate through difficult market conditions.

With this in mind, I’ve set a target price range of RM3-4 for Pchem, and I’m prepared to take action if the stock falls into that range. I’m even willing to take profits or cut losses on some of my smaller, lower-weighted holdings to seize this opportunity. I see it as a once-in-a-lifetime chance, similar to the oversupply situation we saw in the glove industry, which has already proven to be a game-changer.

Maybank IB expects three-year petrochemicals oversupply; keeps ‘sell’ call on PetChem, LCTitan

STOCKS I HAVE MY EYES ON

(MY) YTLPOWER - Malaysia's 1st Independent Power Producer

(MY) PCHEM - Malaysia's Leading Integrated Chemicals Producer

(MY) YINSON - Global Energy Infra. & Technology Firm

(MY) NATIONGATE - Electronics Manufacturing Services Provider

(MY) ATECH - Electronics Manufacturing Services Provider

(US) HERSHEY - Chocolate Snack Producer

(US) ASML - Monopoly for Lithography Machines

(US) KNSL - Specialty Insurance Company

(AS) KPG - Australian-based chartered Accounting Firm